First Home Buyer

Residential Home Loans

Investment Loans

Commercial Products

About Neomoney

Contact Neomoney

📈 Neomoney 2026 Rate Review Guide.

Navigating the 4.10% Cash Rate & Protecting Your Wallet.

With the RBA Cash Rate officially hitting 4.10%, variable-rate borrowers are feeling the squeeze. If you’ve been with the same lender for more than 12 months, you are likely paying a “Loyalty Penalty” meaning new customers are getting better rates than you.

At Neomoney, our philosophy is simple: Don’t wait and see. Review and save.

🔍 Step 1: Know Your Numbers

Before you can improve your rate, you need to know exactly where you stand. Grab your latest mortgage statement or open your banking app and locate:

- Your Current Interest Rate: (Is it starting with a 5.xx%, 6.xx%, 7.xx% or higher?)

- Your Outstanding Loan Balance

- Your Remaining Loan Term: (e.g., 22 years, the remaining years or months to pay down your loan)

- Your Current Property Value: (A rough estimate of what your home is worth today). If you don’t know, not to worry we can help with that once we eventual talk with each other.

Why this matters: Your current property value divided by your loan balance gives you your Loan-to-Value Ratio (LVR). If your home has gone up in value, your LVR has dropped, which unlocks access to “Equity” and lower, highly competitive market rates.

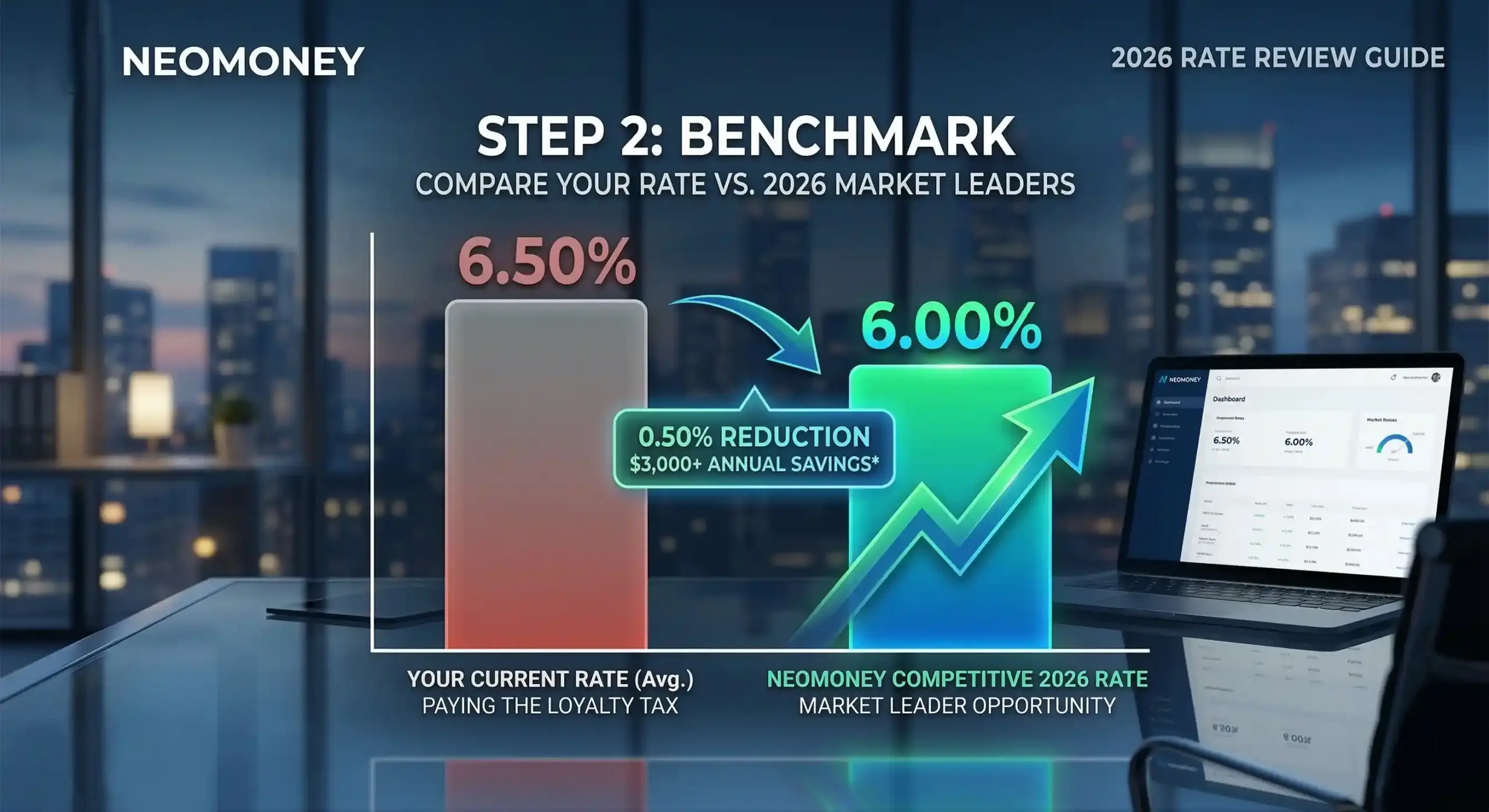

💡 Step 2: Benchmark Against the 2026 Market

Banks rely on you being too busy to check the market. Right now, lenders are fighting for good borrowers.

- The “Loyalty Penalty”: The difference between the rate you are paying and the rate a bank offers a new customer can be up to 0.50% or more.

- The Math: On a $600,000 mortgage, a 0.50% reduction in your interest rate could save you over $3,000 a year in interest alone.

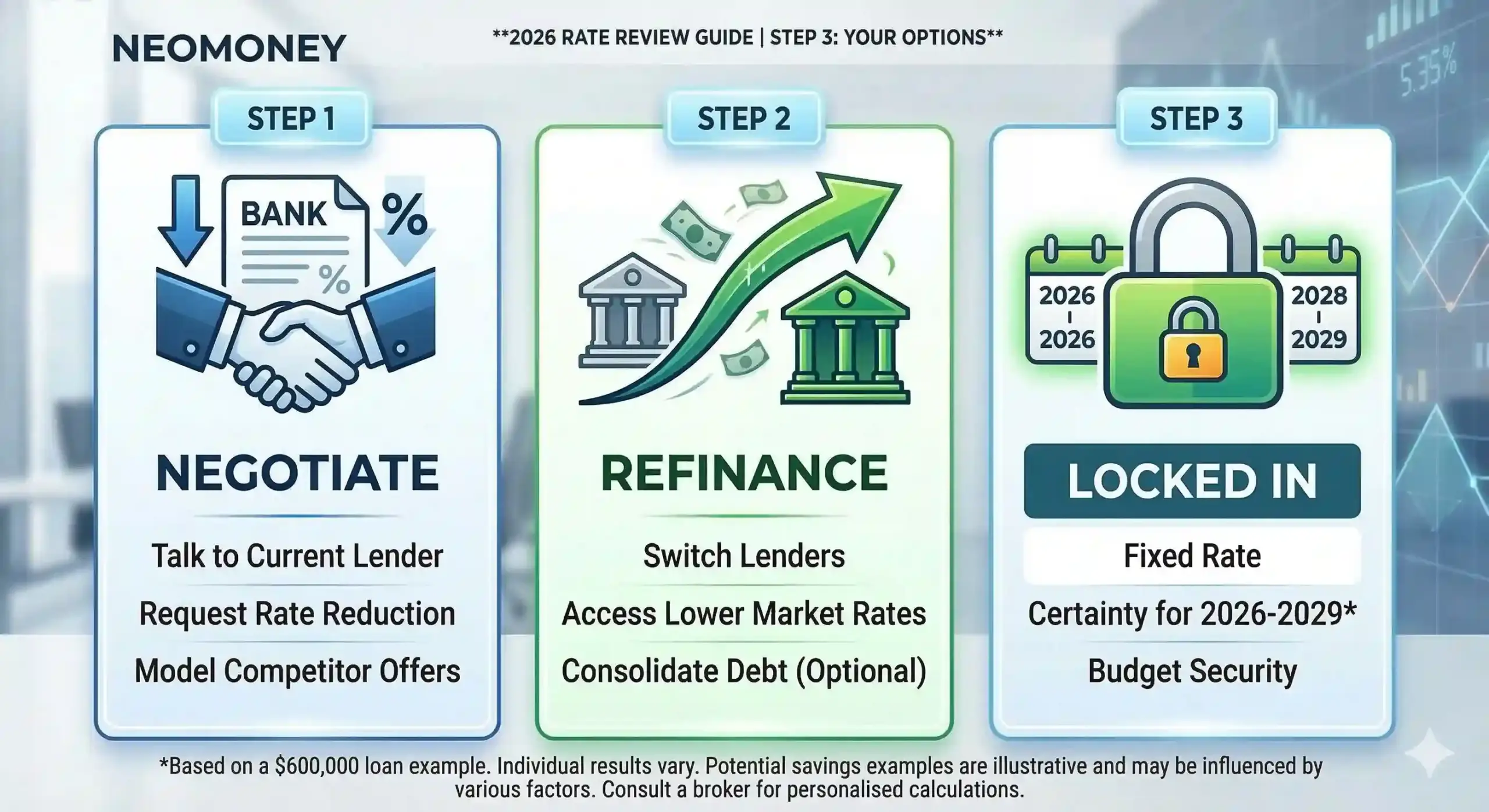

🛠 Step 3: The 3 Options You Have Right Now

1. Negotiate

Sometimes, a simple phone call asking for a rate reduction (armed with competitor rates) is all it takes.

(You can do this by calling your lender and asking for a rate review!)

2. Refinance

If your current bank won’t budge, they we discuss your options to take your loan to a lender that will. We manage the paperwork and negotiate the transition to a lower variable rate.

3. Fix the Rate

If budgeting certainty is your number one priority in this fluctuating market, fixing a portion or all of your loan might be the right strategy.

🚨 The Cost of “Waiting and Seeing”

Every month you put off reviewing your rate, you are handing extra money directly to the bank. Interest rates compound, which means a slightly higher rate today costs you exponentially more over the 25 to 30 year life of your loan.

✅ Next Steps: Let Neomoney Run the Numbers

You don’t need to spend hours comparing comparison rates, calling banks, or reading the fine print.

That is exactly what we do at zero cost to you.